For over 5 years now, I have dedicated my career to studying the patterns and principles that separate the financially thriving from those who constantly struggle. I’ve worked with budgets, analyzed investment portfolios, and watched market cycles across different economies, but the most profound realization I’ve gained isn’t about picking the right stock; it’s about mastering the best money habits.

We all want to know the secret to financial success. The truth is, there isn’t one magic secret. Instead, financially successful people around the world from the bustling streets of Mumbai and Delhi to the financial districts of New York, London and Sydney all share a surprisingly similar set of core daily actions. These are the practical money habits that pave the path to wealth creation, regardless of your income level or where you live.

In this deep dive, I’m sharing the 7 most impactful money habits I have observed and personally adopted. Whether you’re a recent graduate in India looking to build your first corpus, or a professional in a Tier 1 country aiming for early retirement, mastering these daily financial disciplines is your foundational roadmap to lasting security. Let’s explore these wealth-building routines and learn how you can integrate them into your life, starting today.

Table of Contents

ToggleWhat are the best money habits of financially successful people?

The best money habits of financially successful people are rooted in conscious spending and automatic saving. They consistently pay themselves first (automating savings and investments), meticulously track their spending without judgment, adopt a growth mindset focused on increasing income and practice delayed gratification. They also prioritize debt elimination and regularly review their financial plan (at least quarterly) to maintain their long-term trajectory toward financial independence.

The 7 Best Money Habits of Financially Successful People

1. Always Pay Yourself First

This is perhaps the most fundamental principle separating those who save from those who just wish they could save. Financially successful people don’t save what’s left over after expenses; they allocate a portion of their income to savings and investments before paying any bills.

The mindset shift is crucial: you are treating your future self as your most important creditor. By automating your savings and investments, you eliminate decision fatigue and prevent money from being eroded by lifestyle creep or discretionary spending.

Tier 1 & India Angle: In the US, this means maximizing your 401(k) or Roth IRA contributions. In India, this means setting up a Systematic Investment Plan (SIP) in mutual funds or contributions to a Public Provident Fund (PPF) to happen automatically on the day your salary hits your account. This is the easiest way to build wealth without relying on willpower. I use this habit daily to ensure my financial goals are met, treating my investment contributions like a non-negotiable utility bill.

- The concept of building wealth often starts with the power of compounding. Read our guide on The Eighth Wonder of the World: Harnessing the Power of Compounding.

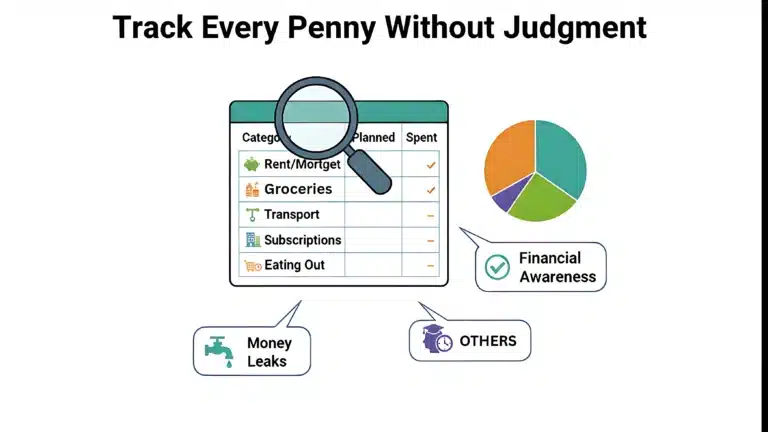

2. They Track Every Penny Without Judgment

Many people hate budgeting because they view it as restrictive. Financially successful people view expense tracking as a tool for financial awareness, not a tool for guilt. They track how to track expenses effectively to identify where their money is actually going versus where they think it’s going. This is the difference between blindly spending and conscious spending.

The goal of this habit is to uncover the “money leaks”—the small, recurring charges (like subscription services) or the areas of overspending (like takeout) that silently erode wealth. Once you have a clear picture, you can make informed, data-driven decisions on where to cut, not emotional ones.

Tier 1 & India Angle: For those in Tier 1 countries, apps like YNAB (You Need A Budget) or Mint are popular. For the Indian audience, using simple spreadsheet trackers or apps that categorize spending based on SMS alerts can be hugely effective. I use expense tracking quarterly to uncover hidden subscription costs and re-evaluate my spending against my long-term goals.

- Once you’ve tracked your expenses, a great way to implement a sustainable spending plan is by utilizing the 50/30/20 Rule. See our guide on The 50/30/20 Rule Explained: A Beginner’s Guide to Smarter Budgeting.

3. Prioritize High-Interest Debt Elimination

Debt is a tool, but high-interest debt (like credit card debt or expensive personal loans) is a financial liability that acts as a powerful brake on wealth creation. Financially successful people recognize that stop paying unnecessary interest is the best guaranteed return on investment you can get.

The money they would have invested is temporarily redirected to aggressively pay down high-interest balances. They understand that every dollar paid in 20% credit card interest is a dollar that cannot compound for them in the stock market.

Tier 1 & India Angle: Whether you are facing high credit card APRs in the US or expensive short-term loans in India, the strategy remains the same. I advise utilizing the Debt Avalanche method (paying the highest interest rate first) as it is the fastest and most mathematically efficient way to clear debt. We all know debt snowball vs debt avalanche explained clearly shows the long-term benefit of tackling the highest rates first.

4. Adopt a "Growth Mindset" Focused on Income

There is a ceiling on how much you can save, but there is virtually no ceiling on how much you can earn. Financially successful people don’t just focus on frugality; they adopt a growth mindset centered on increasing income. They understand that a 10% raise or a successful side hustle will generate far more wealth over a lifetime than cutting a $5 coffee habit.

This habit involves constant learning, skill acquisition, and career negotiation. It’s about viewing your income as a lever, not a fixed dial. The goal is to build wealth from both sides of the equation: maximizing cash inflow while optimizing cash outflow.

Tier 1 & India Angle: In Tier 1 countries, this often means negotiating your salary annually and building a diversified income portfolio with a side hustle. In India, where income growth rates can be significant but competition is high, this means continuous upskilling (coding, digital marketing, data analysis) to command higher salaries. My experience shows that income growth is often the fastest path to significant wealth accumulation.

5. Practice Deliberate and Delayed Gratification

The modern consumer economy is built on instant gratification. Financially successful people resist the urge for quick fixes and implement the habit of delayed gratification for financial success. They put friction between their desire to buy and the actual purchase.

A common tactic is the “48-Hour Rule,” where they impose a mandatory two-day waiting period before buying anything non-essential over a certain rupee or dollar amount. This cooling-off period is enough to diffuse the emotional high of impulse buying and ensure the purchase aligns with their long-term values.

Tier 1 & India Angle: This is key to fighting “lifestyle inflation” where rising income is immediately matched by rising expenses. Whether it’s resisting the urge for the latest iPhone in San Francisco or the newest car model in Delhi, the principle is identical: buy freedom now by saving, instead of buying things now that delay your freedom.

- To fight this, understand the triggers of emotional spending. Learn Emotional Spending: How to Spot Your Triggers and Stop Buying Happiness.

6. They Consistently Invest in Themselves

The highest return on investment (ROI) you will ever find is in your own mind and skill set. Financially successful people are perpetually curious and make investing in financial education a lifelong habit. This is not just about finance; it’s about any skill that increases your value in the marketplace.

They read industry-specific books, take courses to learn a new programming language, or join professional networking groups. This investment fuels Habit 4 (Income Growth), creating a positive feedback loop where skills lead to higher income, which leads to more capital to invest, and so on.

Tier 1 & India Angle: In Tier 1 countries, continuous professional development is expected. In India, where competitive exams and certifications drive career mobility, this habit is non-negotiable. It’s about seeing yourself as a business that requires continuous R&D. I believe this habit offers the highest long-term ROI in the pursuit of wealth.

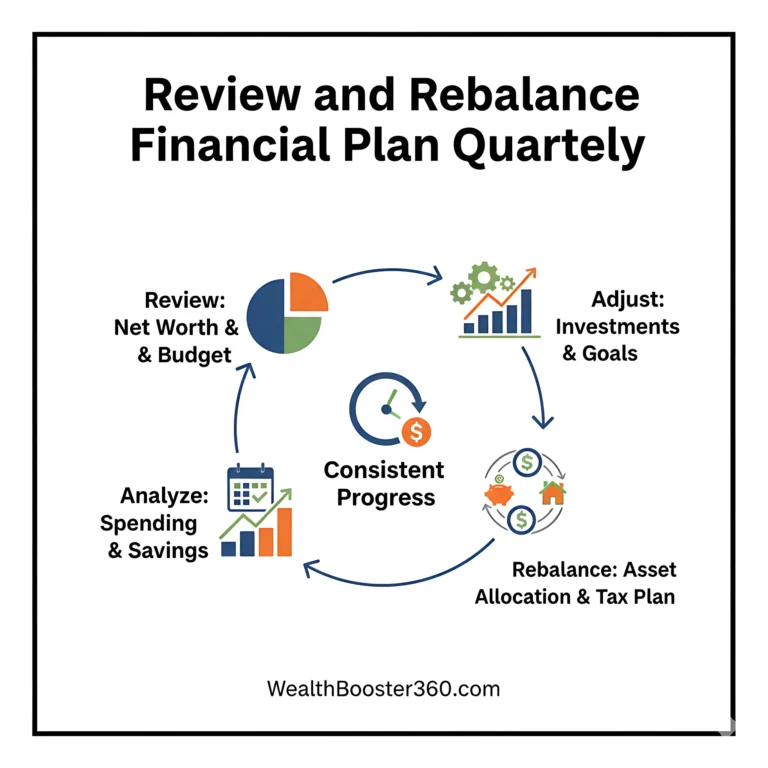

7. Review and Rebalance Their Financial Plan Quarterly

Failing to plan is planning to fail. The final core habit is the intentional act of scheduling a quarterly financial review checklist. Successful people don’t just set a plan and forget it; they treat their personal finances like a CEO treats a business plan.

This quarterly ritual includes:

-

Checking their net worth statement.

-

Reviewing their budget for the last three months.

-

Rebalancing their investments to ensure they haven’t become too heavily weighted in one asset class (like stocks) due to market growth.

-

Adjusting their savings and investment contributions based on their goals.

Tier 1 & India Angle: Regular reviews are critical in volatile markets and for managing tax efficiency. In the US, this is the time to check on IRA limits. In India, it’s when you re-evaluate your SIP allocation and ensure your tax-saving investments (like ELSS) are on track for Section 80C benefits.

Conclusion:

The journey to becoming one of the financially successful people you admire isn’t paved with complex stock market secrets; it’s paved with daily discipline. After my 5+ years in this niche, I can confidently tell you that these 7 best money habits are the universal building blocks. They work in London, they work in Bangalore, and they will work for you.

Your financial future is built on what you do today. Don’t try to implement all seven at once pick the one that resonates most, master it, and then build on that momentum. Remember, success in finance is a marathon of consistency, not a sprint of intensity.

🚀 Ready to Transform Your Financial Future?

I’ve shared my experience and the 7 best habits now it’s your turn to act.

Head over to WealthBooster360.com to explore our library of beginner-friendly guides on budgeting, investing, and wealth creation designed for global success.

If this article helped demystify the best money habits, please share it with a friends and family member who needs this roadmap! Also, I’d love to hear from you: What is the single best money habit you currently practice? Leave a comment below and share your wisdom with our community.

Frequently Asked Questions (FAQs)

Q1. Is it too late to start developing good money habits?

Ans. No, The best time to start was yesterday; the next best time is today. Financial success is built through consistent, small habits, not one-time actions. Even in my 5+ years of advising on finance, I’ve seen people pivot their financial future in their 30s, 40s, and 50s simply by applying these core disciplines. Your financial journey is uniquely yours, and the habits you adopt today will define tomorrow.

Q2. How long does it take to see results from new money habits?

Ans. You will notice a shift in your mindset and stress level within 30 days. Measurable financial results, such as reduced debt or a growing investment portfolio, typically start becoming noticeable after 6 to 12 months of consistent application of the best money habits. Consistency is the key ingredient that turns habit into wealth.

Q3. What is the single most important habit for wealth creation?

Ans. While all 7 money habits are crucial, the single most important habit for wealth creation is Habit 4: Adopting a “Growth Mindset” focused on increasing income. There is a ceiling on how much you can save, but there is virtually no ceiling on how much you can earn. Increasing your earning power gives you more capital to automatically save and invest, making income generation the ultimate leverage point.