Table of Contents

ToggleIntroduction: From Financial Overwhelm to Freedom

Are you Struggling to save money despite earning what seems like a decent salary? You’re certainly not alone. The overwhelming majority of people fall into the trap of letting their expenses dictate their financial future, resulting in the dreaded “paycheck-to-paycheck cycle.” The problem isn’t always the amount of money you earn; it’s the lack of a simple, workable structure for where that money goes.

The word “budgeting” often triggers images of meticulous tracking, complex spreadsheets and feeling guilty about every small purchase. This is precisely why most conventional budgets fail. They are too restrictive and too complicated for the average person to maintain long-term.

Fortunately, there’s a better way. Enter the 50/30/20 rule: a remarkably simple and flexible budgeting rule that has become a cornerstone of modern personal finance tips. It’s a powerful framework that doesn’t just manage your money, it fundamentally shifts your financial priorities, ensuring you are saving for the future while still enjoying the present. This article serves as your ultimate beginner budgeting guide to mastering the 50/30/20 rule and finally learning how to save money with consistency.

What is the 50/30/20 Rule?

The 50/30/20 rule is a percentage-based budgeting method popularized by U.S. Senator Elizabeth Warren and her daughter, Amelia Warren Tyagi, in their book, All Your Worth: The Ultimate Lifetime Money Plan.

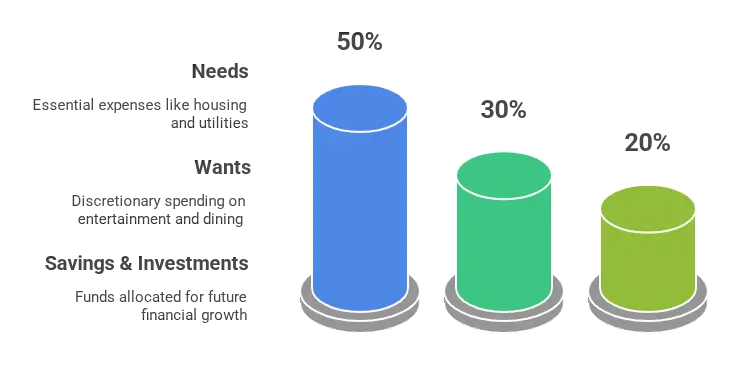

It dictates that you divide your after-tax income (the money that actually lands in your bank account after all taxes and mandatory deductions) into three simple buckets:

- 50% for Needs (The Essentials)

- 30% for Wants (The Discretionary Spending)

- 20% for Savings & Investments (The Financial Future)

The genius of this framework is that it instantly shows you where your money should be going, acting as an automatic financial check-up every single month. If your biggest expense—housing—is eating up 60% of your income, the 50/30/20 rule instantly tells you that you have a fundamental problem with your fixed expenses that needs correcting.

In-Depth Breakdown: The Three Pillars

To effectively use this budgeting rule, you must have crystal-clear definitions for each of the three categories. Misclassifying an expense is the most common reason the 50/30/20 rule fails.

1. 50% for Needs (The Non-Negotiables)

Needs Category | Why It’s a Need |

Housing (Rent/Mortgage EMI) | Shelter is fundamental. Note: The minimum EMI should be here, extra payments go to Savings. |

Basic Groceries | Food required for daily survival and nutrition (rice, milk, vegetables). |

Utilities | Essential services like electricity, water, gas, and a basic mobile/internet connection required for work. |

Minimum Loan Payments | The legally required minimum payments on debt (student loans, car loan EMI, credit card minimums). |

Transportation | Fuel, basic transit passes, or the minimum cost to get to work. |

Insurance | Health insurance, term life insurance, and car insurance premiums. |

The 50% bucket is dedicated to your essential, mandatory expenses. These are the costs necessary for survival and maintaining your job.

Housing (Rent/Mortgage EMI): Shelter is a fundamental need. Note that only the minimum required EMI should be included here; any extra principal payments should be allocated to the 20% Savings category.

Basic Groceries: This includes food required for daily survival and nutrition (e.g., rice, milk, vegetables), not gourmet or specialty items.

Utilities: Essential services like electricity, water, gas, and a basic mobile/internet connection required for your work.

Minimum Loan Payments: These are the legally required minimum payments on existing debt, such as student loans, car loan EMIs, or credit card minimums.

Transportation: This covers the fuel, basic transit passes, or minimum cost required to travel to and from work.

Insurance: Premiums for essential coverage like health insurance, term life insurance, and basic vehicle insurance.

Key Distinction: It’s important to differentiate between basic needs and premium versions of needs. A basic internet connection is a need; a premium fiber-optic connection for gaming is a want.

2. 30% for Wants (The Lifestyle Enhancers)

The 30% bucket is dedicated to discretionary spending—the things you buy to improve your life, provide enjoyment, or for convenience. These are expenses you could theoretically cut to zero without affecting your survival or job.

Wants Category | Why It’s a Want |

Entertainment | Netflix, Amazon Prime, Spotify subscriptions, movie tickets, concerts. |

Dining Out / Takeout | Meals at restaurants, grabbing coffee from a cafe, ordering in food. |

Non-Essential Shopping | New clothes (when you already have enough), gadgets, home decor. |

Premium Services | Gym memberships, expensive hobbies, beauty salon visits, maid service. |

Vacations & Travel | All costs related to holidays, weekend getaways, and non-work travel. |

The 30% bucket covers discretionary spending—the expenses you incur for enjoyment, convenience, or to enhance your lifestyle. These are items you could technically cut to zero without affecting your ability to survive or maintain your job.

Entertainment: This includes all non-essential subscriptions like Netflix, Amazon Prime, and Spotify, as well as movie tickets or concert fees.

Dining Out / Takeout: Any money spent on meals at restaurants, grabbing coffee from a café, or ordering in food falls here.

Non-Essential Shopping: Buying new clothes (when your old ones are still functional), purchasing gadgets purely for pleasure, and spending on home décor are all “wants.”

Premium Services: This includes gym memberships, fees for expensive hobbies, regular beauty salon visits, or the cost of a maid service.

Vacations & Travel: All costs related to holidays, weekend getaways, and non-work-related travel are funded by this category.

The purpose of the 30% bucket is to provide a “guilt-free” spending allowance. By budgeting for fun, you avoid feeling deprived, which is the secret to long-term adherence to this budgeting rule.

3. 20% for Savings & Investments (The Future You)

This is arguably the most crucial bucket. The 20% is the portion of your income that is explicitly directed toward building your financial future.

Savings & Investment | Why It’s a Priority |

Emergency Fund Contributions | Building a cash reserve (3-6 months of living expenses). |

Retirement Investments | Contributions to 401(k), PPF, mutual funds, stocks, or retirement accounts. |

Long-Term Goal Savings | Saving for a house down payment, a child’s education, or a new car. |

Extra Debt Repayment | Any payment above the required minimum on a high-interest loan (e.g., credit card debt). |

This is the most crucial pillar, dedicated to building your future wealth and financial security. This money is explicitly directed toward long-term goals.

Emergency Fund Contributions: This includes building a cash reserve designed to cover 3-6 months of your living expenses in case of job loss or a medical emergency.

Retirement Investments: Any contributions made to formal retirement vehicles like a 401(k), PPF, mutual funds (SIPs), or purchasing stocks for the long term fall into this category.

Long-Term Goal Savings: Money set aside for major future purchases, such as a down payment for a house, a child’s education fund, or saving up for a car in cash.

Extra Debt Repayment: Any payment made above the minimum required on a high-interest loan (like credit card debt or personal loans) is a form of saving, as it significantly reduces future interest costs.

The 50/30/20 rule makes savings non-negotiable. It forces you to “pay yourself first,” a fundamental tenet of sound personal finance tips.

Why the 50/30/20 Rule is the Best Beginner Budgeting Guide

The effectiveness of this rule as a beginner budgeting guide stems from several psychological and practical advantages:

- It Promotes Immediate Financial Discipline: By setting the 50% limit on Needs, the rule forces you to make conscious choices about your fixed costs. If your rent is too high, the rule highlights the issue instantly, compelling you to correct your lifestyle to fit your income.

- It is Anti-Deprivation: The dedicated 30% “Wants” allowance prevents the burnout common in other restrictive budgets. Knowing you have money set aside for fun makes the process enjoyable and sustainable.

- It is Action-Oriented: The goal of the 20% is clear: future building. This encourages to move beyond just saving cash to actively investing, thereby teaching how to save money that grows over time through compounding.

Step-by-Step: How to Implement the 50/30/20 Rule Today

Mastering the rule is a simple three-step process:

Step 1: Calculate Your True Income (Net Income)

Do not use your gross salary. Your 50/30/20 rule budget must be calculated using your net monthly income (your take-home pay). This is the amount you actually have control over. For irregular incomes (freelancers, business owners), use a conservative average of the last six months as your baseline.

Step 2: Audit Your Current Spending

Go through your bank statements, credit card bills, and payment apps for the last two or three months. Categorize every single expense into Needs, Wants, or Savings. This audit is crucial:

- Are your current Needs at 55%? You have a 5% fixed cost problem.

- Are your Wants at 40%? You need to cut discretionary spending by 10% immediately.

Step 3: Automate, Automate, Automate

The most effective personal finance tips involve automation. On the day you get paid:

- Automate 20% of your paycheque to immediately transfer to your dedicated savings or investment accounts. By paying yourself first, you ensure this money is never accidentally spent.

- Leave 50% for fixed bills (Needs).

- Transfer the remaining 30% to a separate spending account to be used solely for Wants. This makes it a hard limit for your fun spending.

Real-Life Application: Seeing the Rule in Action

The 50/30/20 rule makes sense when you see it applied to real-world salaries.

Example with a ₹30,000 Monthly Net Income:

Category | Calculation (₹) | Specific Allocation Examples (Needs) |

50% Needs | ₹15,000 | Rent: ₹7,000; Groceries: ₹3,500; Utilities/Phone: ₹2,000; Minimum Loan EMI: ₹2,500. |

30% Wants | ₹9,000 | Dining Out: ₹3,000; Clothing/Shopping: ₹2,000; Entertainment/Subscriptions: ₹1,000; Miscellaneous Fun: ₹3,000. |

20% Savings/Investments | ₹6,000 | SIP in Mutual Fund: ₹3,000; Emergency Fund: ₹2,000; Extra Loan Repayment: ₹1,000. |

Total Income | ₹30,000 |

With a net monthly income of ₹30,000, here is how the 50/30/20 rule dictates your spending:

50% Needs (₹15,000): This allocation covers essentials like Rent (₹7,000), Groceries (₹3,500), Utilities/Phone (₹2,000), and the Minimum Loan EMI (₹2,500).

30% Wants (₹9,000): This allows for flexibility and fun, including Dining Out (₹3,000), Clothing/Shopping (₹2,000), Entertainment/Subscriptions (₹1,000), and other Miscellaneous Fun (₹3,000).

20% Savings/Investments (₹6,000): This is the future-building component, allocated to a SIP in a Mutual Fund (₹3,000), contributions to an Emergency Fund (₹2,000), and potentially an Extra Loan Repayment (₹1,000).

- Insight: Even on a moderate salary, the disciplined investor is channeling ₹6,000 monthly toward their financial future. This consistency is how wealth is built.

Example with a ₹50,000 Monthly Net Income:

Category | Calculation (₹) | Specific Allocation Examples (Needs) |

50% Needs | ₹25,000 | Rent/Mortgage EMI: ₹14,000; Groceries: ₹6,000; Utilities/Insurance: ₹5,000. |

30% Wants | ₹15,000 | Dining Out/Takeout: ₹5,000; Hobbies/Gym: ₹3,000; Shopping/Gadgets: ₹4,000; Travel Savings: ₹3,000. |

20% Savings/Investments | ₹10,000 | Retirement Fund (PPF/NPS): ₹5,000; Equity Mutual Fund SIP: ₹4,000; Emergency Fund: ₹1,000. |

Total Income | ₹50,000 |

Example with a ₹50,000 Monthly Net Income

With a higher net monthly income of ₹50,000, the absolute amounts increase, accelerating your goals:

50% Needs (₹25,000): This higher allocation allows for a higher standard of fixed living, such as Rent/Mortgage EMI (₹14,000), a larger budget for Groceries (₹6,000), and Utilities/Insurance (₹5,000).

30% Wants (₹15,000): This provides a significant allowance for lifestyle upgrades, including Dining Out/Takeout (₹5,000), Hobbies/Gym (₹3,000), Shopping/Gadgets (₹4,000), and dedicated Travel Savings (₹3,000).

20% Savings/Investments (₹10,000): This substantial amount can be allocated aggressively, such as for a Retirement Fund (PPF/NPS) (₹5,000), an Equity Mutual Fund SIP (₹4,000), and an Emergency Fund contribution (₹1,000).

- Insight: As income increases, the 20% savings component becomes substantial (₹10,000), accelerating wealth building. The 30% allowance for Wants allows for a significant upgrade in lifestyle without compromising the future.

Limitations and Customizing Your 50/30/20 Rule

No single budgeting method works for every person in every stage of life. The 50/30/20 rule is a template, and smart personal finance involves knowing when to bend it.

- The High Cost-of-Living Hurdle: If you live in a Tier 1 metropolitan area, it is incredibly common for rent alone to exceed the 50% Needs limit. In this scenario, you must adjust the rule by reducing your Wants bucket. A 60/20/20 split (60% Needs, 20% Wants, 20% Savings) is a common and necessary modification.

- The High-Debt Modification: If you are actively paying down high-interest debt (like credit card or personal loans), you need an aggressive savings approach. Consider a 50/10/40 split, where the extra 20% taken from Wants is funneled directly into debt repayment, which is essentially the best form of short-term saving.

- The Aggressive Savings Goal: If you are nearing retirement or saving for a major goal (e.g., buying a house in two years), you might temporarily adopt a 40/20/40 split, sacrificing your current lifestyle for massive future gains.

The ultimate lesson of this beginner budgeting guide is flexibility. Use the 50/30/20 structure to gain clarity, but customize the percentages to fit your current financial reality and your most urgent goals.

Conclusion:

The greatest challenge in personal finance is consistency, and the 50/30/20 rule is the antidote to financial chaos. It is the most effective beginner budgeting guide because it removes guilt, promotes balance, and, most importantly, guarantees that you pay yourself first. By committing to this simple structure, you stop being a financial spectator and start actively directing your income toward the future you deserve. Try it for just one month audit your spending, set your percentages, and automate your savings. The clarity and control you gain will be transformative.

Ready to take control of your money? Check out our Passive Income, Investing for Beginner’s blogs for more Information.

Disclaimer:-

The information presented in this blog post regarding the 50/30/20 rule and general budgeting tips is for educational and informational purposes only. It is not intended to be a substitute for professional financial or tax advice. The rule is a generalized template, and individual results will vary based on personal income, debt levels, cost of living, and spending habits. You should always consult with a qualified financial advisor, accountant, or tax professional to discuss your specific financial situation before making any significant budgeting, spending, or savings decisions. The author and publisher are not liable for any financial losses or damages resulting from the use of this information.

FAQs (Frequently Asked Questions)

Q1: Do I calculate the 50/30/20 rule based on Gross or Net Income?

You should always calculate the 50/30/20 rule based on your Net Income (your take-home pay) after taxes and mandatory deductions (like PF contributions) are taken out. This represents the actual money you have control over each month.

Q2: Is paying off debt a 'Need' or 'Savings'?

Minimum debt payments (the EMI you must pay) are a Need (50%). Any extra payment made above the minimum requirement to accelerate debt freedom is considered Savings (20%), as it’s directly building your future financial security by reducing interest payments.

Q3: What if my Needs are already over 50%?

This means your fixed expenses are too high for your current income. You need to adjust your budget, often by reducing your Wants (30%) to a lower percentage (e.g., creating a 60/20/20 split) or, ideally, finding ways to lower your Needs (e.g., moving to a cheaper apartment or reducing a large EMI).

Q4: Can I use the 30% 'Wants' money for Investments instead?

Absolutely! The 30% is your flexible category. If your primary goal is aggressive wealth building (like achieving FIRE), diverting some or all of your ‘Wants’ money into the ‘Savings & Investment’ bucket is a common and powerful personal finance tip that accelerates your timeline.

FIRE= Financial Independence Retire Early.